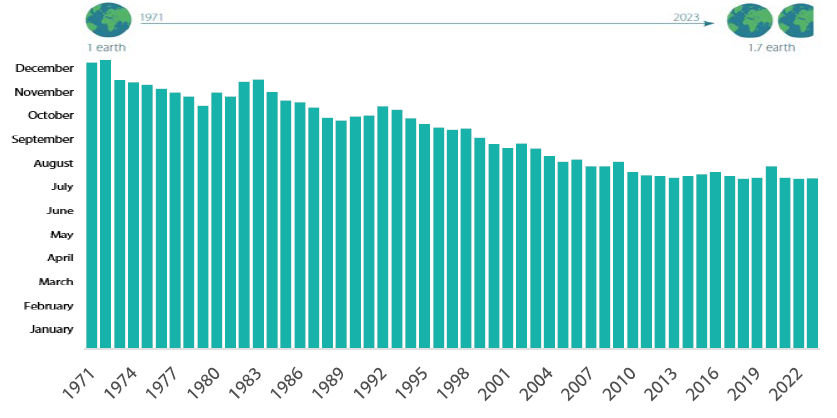

Climate change is not the only environmental threat to how we live, work and interact with our planet. Our economic system is based on a model of take, make and waste that consistently over-utilises and fails to replenish Earth’s valuable, but dwindling resources. This is best depicted by Earth Overshoot Day, the annual date when humanity’s demand for ecological resources and services exceeds what Earth can regenerate in that year (Chart 1).1 In 2023, this fell on 2 August and has been occurring earlier each year.

Chart 1: Progression of Earth Overshoot Day 1971 2023

Source: https://overshoot.footprintnetwork.org/about/

More than just birds and bees…

The plight of bees is often used to illustrate the need to better preserve nature. As nature’s pollinators, bees are a vital part of our food value chain. But their numbers are plummeting as their natural habitat is lost. Yet, biodiversity is about so much more than just bees and birds, it covers all of the planet’s ecosystems, flora and fauna. And each of these components is at risk. More than a million species currently face extinction; since 1970, the wildlife population has declined by 69%.2 Deforestation is another pressing issue—10 million hectares of forest were lost between 2015–2020.3

Nature is also a massive contributor to economic growth. According to PWC, more than half (55%) of the world’s gross domestic product—equivalent to an estimated US dollar 58 trillion—is moderately or highly dependent on nature.4 And the deterioration of natural ecosystems could have far-reaching implications that are often not favoured in business risk analysis at present.

A new direction for green bonds

The need to transform how we interact with nature creates a major opportunity for the green bond universe. So far, issuers have successfully embraced funding the transition toward carbon neutrality, but far fewer are looking at regenerative biodiversity projects or initiatives that seek to protect our ecosystems from loss. As awareness of the biodiversity threat grows, demand will rise from asset owners, especially ESG fixed income strategies that are not exclusively focused on the net zero transition, and also through evolving regulation – the same forces that first built momentum for climate-related green bonds. At this early stage, the biodiversity theme could prove profitable as high demand and limited supply will drive up the greenium5 of these investments. Furthermore, as fixed income risk mitigation strategies factor in the threat to biodiversity, investors will increasingly seek to avoid those companies that threaten biodiversity or heavily rely on nature in their value chains without implementing replenishment strategies.

Investing in new research models

As biodiversity is still a new investment research field, and spans such a multitude of aspects, it could be preferable to approach the topic from different angles. Firstly, companies can be categorised into three different groups:

1) Companies whose activities directly impact biodiversity (i.e., oil & gas, transportation and mining)

2) Companies whose activities depend on biodiversity (i.e., utilities, consumer goods and forest products)

3) Companies that try to improve biodiversity – this group does not necessarily relate to specific sectors but

considers the extent to which companies embed an intrinsic motivation to protect and nurture biodiversity within their business strategies

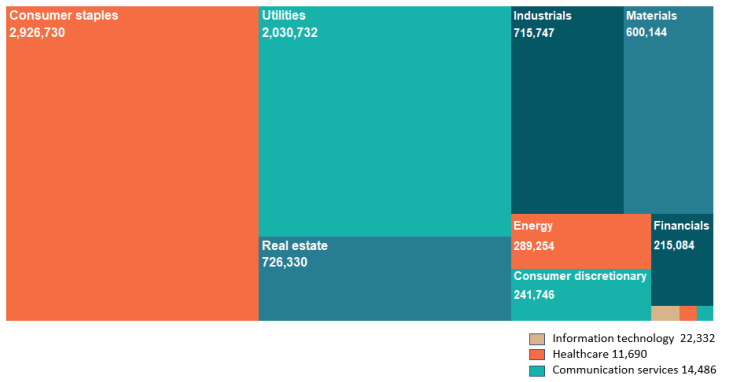

Following this categorisation, measuring impact and dependency is the next logical step. Ratings and research agency S&P presents one way to measure impact/dependency by providing an ecosystem footprint of its proprietary Nature & Biodiversity risk dataset. In its calculations, S&P combines three areas: it measures how land is impacted; ecosystem degradation; and the significance of location-specific ecosystem impacts. According to S&P’s database, consumer staples and utilities have the greatest ecosystem footprint (Chart 2).

Chart 2: S&P’s Nature & Biodiversity Risk Dataset

The consumer staples and utilities sectors have largest ecosystem footprints.

Relative size of ecosystem footprints measure in hectares of Highest Significance Area equivalent by sector for S&P Global BMI companies’ direct operations

Source: S&P Global Sustainable1, data as at 31 March 2023.

In such an emerging area of analysis, any methodologies to assess impact/dependency are only as good as their underlying data. Several new initiatives aim to promote voluntary disclosure standards that factor in biodiversity-sensitive areas as well as all scopes of carbon emissions. So far, the most promising effort has come from the EU, but clearly much work needs to be done in achieving greater transparency in this area.

Meanwhile, detailed commitment from the corporate sector to protect biodiversity is currently lacking. As we have already seen with net zero efforts, only time will tell whether companies voluntarily come forward with biodiversity commitments and action, or if a regulatory push will be needed. In the meantime, investors can play a greater role through engagement initiatives like Nature Action 100 (NA100).6 In October, we were honoured to join NA100’s growing coalition of investors requesting that companies adopt a more radical approach to reduce their reliance on plastics.

As for the asset management industry, we have already seen how successfully it can lead action on climate change and mobilise both investors and companies to engage with this topic. Moving forward, asset managers will have to fine-tune their research efforts relating to the protection of biodiversity, build up reliable databases and support companies with capital by funding genuine projects that seek to restore and replenish our natural world.

1 https://overshoot.footprintnetwork.org/about/

3 PRI, Digital Forum

5Spread difference between a labelled vs. a non-labelled bond