South Korea’s “indie” cosmetics brands: vibrant alternative to large conglomerates

It’s no secret that the global beauty industry has come to be dominated by smaller South Korean players. The “hallyu” wave, also known as the Korean wave, started in the 1990s and ignited the global popularity of South Korean culture and entertainment. Today, this includes beauty trends, blazing a trail across the world with their “K-beauty” skincare and cosmetic products. Terms like “glass skin” have become established globally among the beauty-conscious, along with the 10-step skincare routine prescribed to achieve the hydrated, glowy look.

South Korea may be known for its large conglomerates dominating global industries such as automobiles and semiconductors. But in cosmetics, independently owned and operated South Korean “indie” companies are punching above their weight and making an impact both domestically and globally. An example is iFamilySC Company Limited, which has seen much success through its leading brand Rom&nd. Rom&nd stems from the name of one of Korea’s top beauty creator Saerom Min who founded the brand together with iFamilySC. Launched in 2016, the brand’s success can be attributed to its ability to quickly react to trends, grabbing the attention of the MZ (Millennials and Generation Z ) consumers with their catchy marketing as well as strong product portfolio. Rom&nd is ranked among the top brands in Olive Young, South Korea’s leading health and beauty store chain, for cosmetics as well. The company also actively uses pop-up stores as a marketing channel, something that resonates well with the youth today. Its pop-up store in South Korea, set up in April this year, was estimated to have attracted 40, 000 visitors over 12 days, serving as a good marketing tool. The company is also making waves abroad. According to the media, 300,000 of its cosmetics items stocked at Lawson convenience stores sold out in three days in Japan when Lawson had initially expected the stock to last two months1.

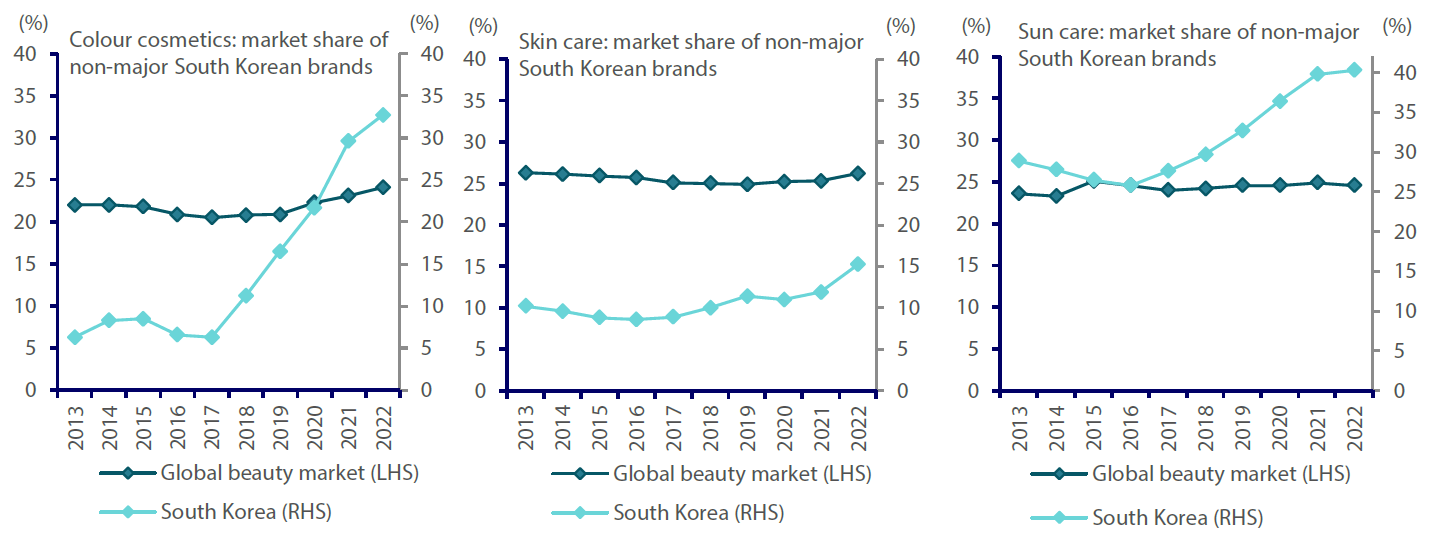

South Korea’s indie cosmetics companies have shown an ability to react quickly and capitalise on changing trends. These small-cap companies have established a presence in South Korean and global cosmetics markets (Chart 1).

Chart 1: South Korea’s “indie” cosmetics companies have seen increasing market share

Source: CLSA, Euromonitor

The main reason for their rapid growth can be attributed to their quick response to market trends and ability to effectively leverage online marketing channels. Silicon 2 Company Limited is one such company that has been facilitating this growth. It operates an online-based K-beauty platform, “stylekorean.com”; it has grown into a leading B2B wholesaler, focusing on distributing independent Korean (K-indie) cosmetics products in the global market, offering more than 300 brands to over 170 countries.

Smaller companies have demonstrated swift response to trends

Successful Asian small caps can be found across the entire region. These companies have shown strong innovation as well as ability to respond quickly to trends. Giant Manufacturing Company Limited in Taiwan, for example, has exhibited adaptability and agility, allowing them to swiftly respond to emerging trends and technological advancements.

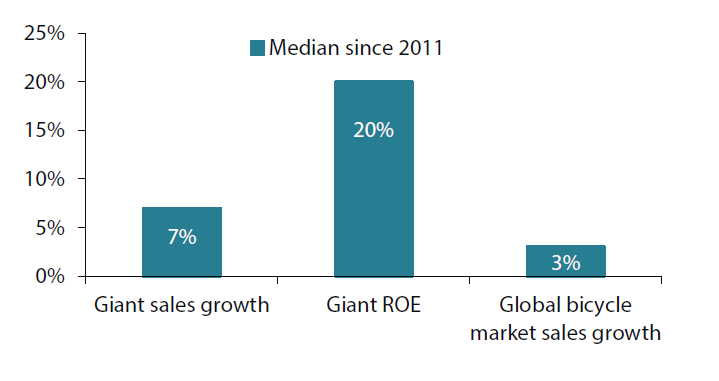

Giant: global leader in a low-growth industry

Giant Manufacturing Company Limited is a leading bicycle manufacturer which has made its mark by becoming a global leader in a low-growth industry. Since 2011, its median sales have been more than twice that of the industry; with a median ROE of 20%, it has demonstrated sustainable returns (Chart 2). Giant’s innovative adoption of technology—it was a pioneer in using carbon fibre and aluminium for bicycles—and its commitment to quality and affordability has made the Taiwanese company one of the largest bicycle manufacturers in the world.

Chart 2: Giant has consistently outperformed the broader industry

Source: Bloomberg, HSBC calculations

Small caps: avenue for sustainable returns and diversification opportunities

In the ever-evolving investment landscape, small-cap stocks in Asia have emerged as a promising avenue for investors seeking sustainable returns and diversification opportunities. These companies operate in markets with huge potential and economic development. In the following paragraphs, we provide other reasons why Asian small-cap stocks warrant the attention of global investors.

Provide access to a large, expanding universe

With over 9,500 small caps2, Asia (excluding Japan, Australia and New Zealand) boasts five times more small-cap stocks than the US. Small caps also play a more prominent role in Asia’s markets. For example, more than 90% of the companies listed in South Korea and Taiwan are small caps, compared to 55% in the US. Furthermore, the universe of listed Asian small caps is experiencing dynamic growth. The number of small caps in Asia has grown by 17% since 2021; in comparison, the US and Japan have seen their small cap numbers each shrink by 7%.

Compared to other global regions, Asia has a bigger universe of small-cap stocks, with these companies often operating in markets rich with untapped potential. These entities provide exposure to regions undergoing substantial economic growth and development.

Best placed to capture fundamental change

Asian small caps offer more than just short-term gains; they strategically position a portfolio for future growth potential by capturing fundamental change, in our view. As these companies evolve and prosper, they stand a chance to become tomorrow's industry leaders. For instance, 15% of the small-cap companies from 2015 have graduated into medium or large-cap status. Moreover, small caps have demonstrated a capacity to generate strong returns, as evidenced by the NIFTY small-cap index in India, which has provided an annualised return of approximately 50% since 2020. India displays a high amount of fundamental change, such as structural reforms in the form of digitisation, as well as growth in infrastructure, which has led to reducing logistics costs (please see "India's transformational trends") .

Using MSCI Asia ex Japan small cap as a base, we can see that small caps offer higher exposure to attractive growth areas such as India at 31% compared to MSCI Asia ex Japan cap index at 20%. By sector, we see small caps having higher exposure to industrials, with 18% compared to only 7% in the large cap index.3 Industrial sectors often experience significant growth during economic expansions and offers exposure to sectors involved in innovation and infrastructure.

Present high growth potential

Asian small-cap companies typically possess significant growth potential. With the rise of emerging markets and economies, these companies are well-positioned to capitalize on expanding consumer bases and increasing demand for products and services.

Earnings growth among Asian small caps has been stronger than that of medium and large caps. Small caps have seen an annualised EPS growth of 10% since 2012, compared to 6% for medium and large caps. India provides an example of small cap outperformance. The country accounts for only a quarter of the small caps in Asia. However, India’s small caps represent roughly half of Asia’s highly profitable small caps with ROEs greater than 20%.

It is worth remembering that 20 years ago Nvidia was a small cap company; today, it has a larger market capitalization than entire stock markets such as those of South Korea and Taiwan. Within Asian small caps, there are many companies displaying high growth and profitability. South Korean semiconductor equipment manufacturer Hanmi Semiconductor is an example of a company that saw its market capitalisation increase from USD 890 million to USD 12.1 billion within 18 months (from January 2023) thanks to robust sales growth. Looking at the universe, 60% of Asian small caps have beaten the FTSE Asia Index excluding Japan, Australia and New Zealand in the last five years.

Give access to simpler corporate structures

Small caps often maintain a simpler corporate structure, focusing on niche markets rather than spanning multiple business units like conglomerates. This simplicity can be more appealing to investors who prefer to invest directly in specific segments and would be willing to pay higher valuation multiples due to the undiluted, stronger growth profile. Domestic investors also tend to invest in small caps within their home markets, as they possess a better understanding of these entities.

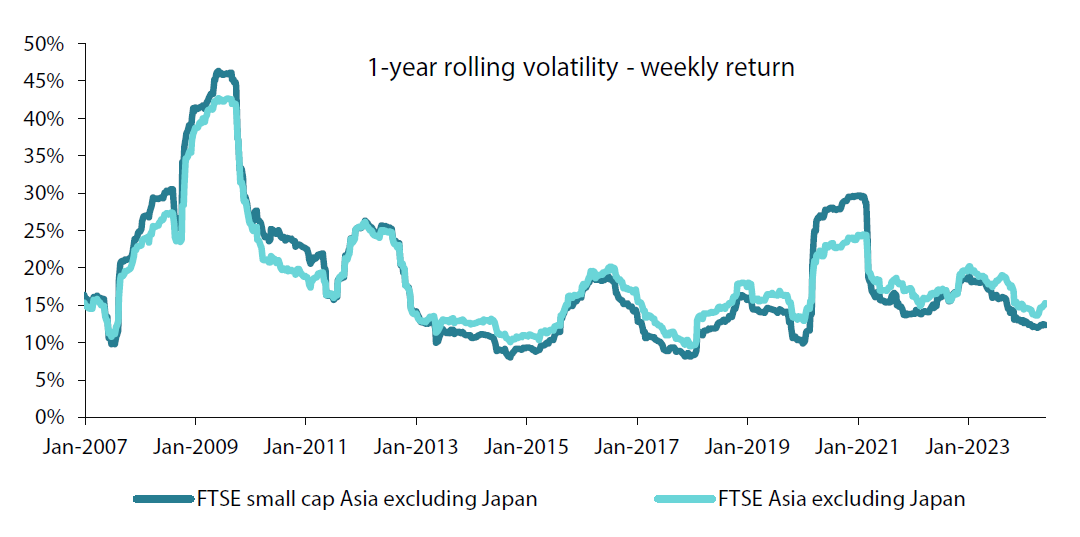

Allow for a balanced risk profile

In our view, having Asian small-cap stocks in the portfolio does not increase the overall portfolio risk and offers higher returns. In the past five years ending May 2024, MSCI Asia ex Japan small caps index has delivered 54.9% returns in USD terms compared to 12.8% for MSCI Asia ex Japan index in USD terms. From Chart 3, we can see that the FTSE Small cap Asia excluding Japan index does not demonstrate significant volatility compared to the FTSE Asia excluding Japan index. By investing in smaller companies, investors can effectively spread their risk and yet retain upside.

Chart 3: Rolling volatility of Asian small caps vs large caps

Source: FTSE Russell, Factset, HSBC

Show ability to outperform under varied conditions

It is a commonly held belief that small-cap stocks tend to outperform only when interest rates are low, and liquidity is ample. Historical data from the US and EU markets seem to corroborate this view, especially during periods when the Federal Reserve and the European Central Bank have raised interest rates, often leading to a less favourable environment for small-cap stocks given the assumption that they carry more debt compared to their larger counterparts.

However, the performance of small caps in Asia challenges this assumption. Despite rising interest rates since 2022, Asian small caps have shown strong outperformance, with the MSCI Asia ex Japan small caps showing 1.93% in USD terms (until May 2024) compared to -9.76% for the MSCI Asia ex Japan in USD terms. We think that this could be attributable to Asian smaller companies having several factors which mitigate the negative impact, such as strong domestic growth, as well as exposure to areas of growth. Key among these are advances in artificial intelligence, shifts in global manufacturing dynamics, and the evolution of consumer habits in the region. In addition, within the small cap universe, we do see companies with strong balance sheets, which reduces the need for financing when rates are high. These factors provide a robust foundation for growth, enabling Asian small caps to thrive even when traditional economic indicators might suggest otherwise.

Summary

Small caps in Asia offer, in our view, an array of opportunities for those seeking high growth potential without significantly changing portfolio risk. These companies, found among emerging markets, present a chance to invest in the future economic powerhouses of the world. The strategic positioning, high growth potential, adaptability, and innovation of Asian small caps make them a compelling choice. Moreover, their simpler corporate structures and balanced risk profiles further enhance their appeal. Despite common misconceptions, Asian small caps have demonstrated consistent outperformance, even under varying market conditions. This underscores their resilience, ability to harness fundamental change and potential for sustainable returns. Therefore, Asian small caps should be seriously considered by investors worldwide in our view.

1 IT Media Business Online, 10 April 2023, Toyo Keizai Online, 2 September 2023

2Companies with market capitalisations of over US dollar (USD) 100 million but less than USD 2 billion

3 MSCI as of May 2024

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way